Foreign Investigation: What It Is, When It Triggers, Penalties, and How to Avoid It in 2026

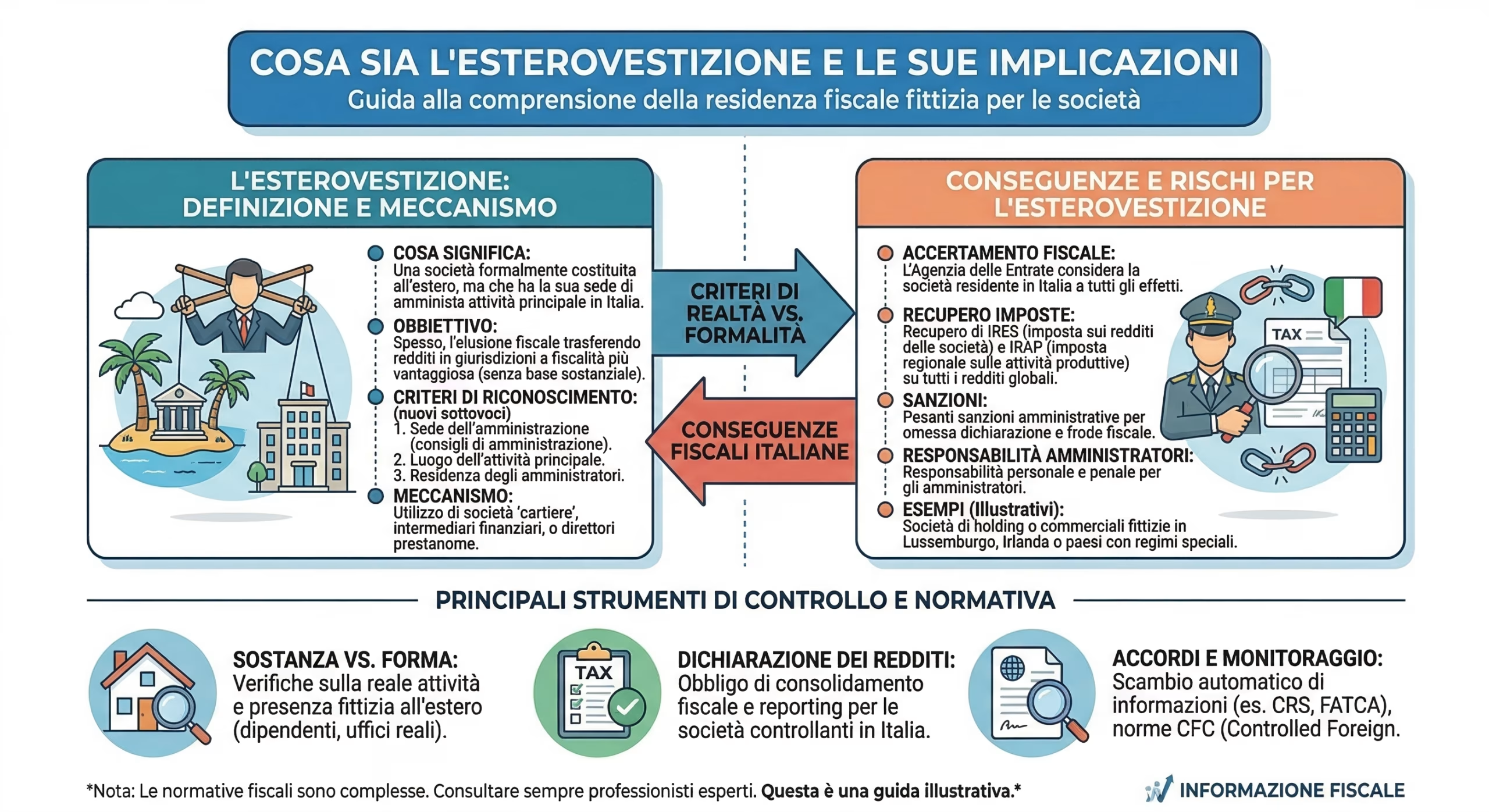

Foreign investiture (foreign investiture) is the fictitious localization of a company or individual's tax residence in a foreign country, while effective management, strategic decisions, and the center of economic interests remain in Italy. The Revenue Agency challenges foreign investiture when a formally foreign entity—a U.S. LLC, a British Ltd, a Panamanian SA, or a Seychelles IBC—has no real economic substance in the country of incorporation and is effectively administered from Italy. The consequences are among the most severe in tax law: IRES and IRAP on all worldwide income, administrative penalties ranging from 120% to 240% of the evaded tax, and criminal liability for amounts exceeding €50,000 per year (Article 4, Legislative Decree 74/2000).

This guide, updated to Legislative Decree 209/2023, Revenue Agency Circular 20/E (November 4, 2024), and the 2024-2025 case law of the Court of Cassation, explains when a company is considered "incorporated abroad," the criteria used by the tax authorities to determine this, the penalties applicable, how it differs from tax evasion and abuse, and the specific structures that allow for fully legitimate operations abroad, without risk of dispute. For Italian entrepreneurs, investors, and professionals who manage or intend to establish foreign companies, particularly in Panama , the United States offshore jurisdictions , this page provides the complete regulatory framework and operational solutions for structuring them correctly.

Regulatory and operational summary

- Definition: fictitious location of tax residence abroad of a company that is effectively managed from Italy (Article 73, paragraph 3, TUIR)

- Assessment criteria (from 2024): registered office, place of effective management, ordinary management in the main street, only one of the three is sufficient

- Legal presumption (art. 73, paragraph 5-bis): a foreign company is presumed to be resident in Italy if it is controlled by Italian entities or has a Board of Directors with an Italian majority, unless proven otherwise.

- Administrative penalties: IRES 24% + IRAP 3.9% on worldwide income + penalty from 120% to 240% for failure to file a tax return

- Criminal relevance: if tax evasion > €50,000/year → false declaration (art. 4, Legislative Decree 74/2000), imprisonment from 2 to 4 years and 6 months

- New for 2024: Legislative Decree 209/2023 has replaced "administrative headquarters" with "effective management headquarters" and "ordinary management in the main street", Circular 20/E has clarified the new criteria

- How to avoid it: actual transfer of the owner's tax residence + economic substance of the company in the foreign country + CFC compliance

What is foreign investiture: legal definition

"Esterovestizione" (foreign investment), a term not codified but consolidated in tax practice and case law, refers to the situation in which a company, despite being formally incorporated and registered in a foreign country, must be considered tax resident in Italy because its effective management takes place in Italy. The legal basis is Article 73, paragraph 3, of the Consolidated Income Tax Code (TUIR ) (Presidential Decree No. 917 of 22 December 1986), which establishes the criteria for determining the tax residence of companies and entities. The term is used both by the Revenue Agency in circulars and tax assessment notices and by the Court of Cassation in rulings on international taxation.

Foreign tax residency is not a separate crime: it is a tax classification that carries sanctions. The Revenue Agency, upon contesting foreign tax residency, reclassifies the company's tax residence as Italian and proceeds to recover taxes (IRES, IRAP, VAT) on all worldwide income generated by the company in the years under assessment, applying the penalties applicable for failure to file a tax return.

Corporate tax residency criteria: Article 73 of the TUIR after the 2024 reform

Article 73, paragraph 3, of the TUIR , as amended by Article 2 of Legislative Decree No. 209 of 27 December 2023 (international tax reform), establishes that a company or entity is considered tax resident in Italy if, for the majority of the tax period (183 days, 184 in leap years), it has even just one of the following elements in the territory of the State:

Registered office

The registered office is the location indicated in the company's articles of incorporation and bylaws. It is a formal criterion: a company with its registered office in Italy is resident in Italy, regardless of where it conducts business. This criterion is rarely disputed because it is objective and documented. The problem of foreign ownership arises when the registered office is abroad but the actual management is in Italy.

Place of effective management

This is the central criterion of the 2024 reform and the most relevant for foreign investments. Revenue Agency Circular 20/E (November 4, 2024) defines the place of effective management as the place where "the continuous and coordinated adoption of strategic decisions regarding the company as a whole" takes place. Strategic decisions include: approval of financial statements, appointment and dismissal of directors, definition of commercial and investment policies, conclusion of significant contracts, decisions on mergers, acquisitions, disposals, and extraordinary transactions.

This criterion replaces the previous reference to "place of management," which had generated significant interpretative difficulties. The distinction is important: the place of effective management concerns high-level strategic decisions , not day-to-day operational management. A foreign company whose CEO resides abroad and makes strategic decisions abroad is not classified as "esterovestita" (incorporated abroad), even if it has an operational office in Italy for ancillary activities.

Ordinary management on the main street

This is the second criterion introduced by the reform. It refers to the location where current management activities are carried out: operational coordination, personnel management, customer and supplier relationships, and ordinary financial transactions. Circular 20/E clarifies that this criterion is an alternative to the location of effective management and is intended to capture cases in which strategic decisions are formally made abroad but all day-to-day operations are conducted in Italy, a common practice in "foreign-dressed" companies that appoint a foreign director as a front but manage everything from Italy.

Legal presumptions of foreign investiture: art. 73, paragraph 5-bis

Article 73, paragraph 5-bis of the TUIR (introduced by Legislative Decree 223/2006 and confirmed by the 2024 reform) provides two relative presumptions of residency in Italy for foreign companies:

Presumption 1: a foreign company is presumed to be resident in Italy if it is controlled, directly or indirectly (including through a corporate chain), by an entity resident in Italy, and in turn holds controlling interests in Italian companies or has its assets consisting predominantly of assets located in Italy.

Presumption 2: A foreign company is presumed to be resident in Italy if its board of directors (or equivalent body) is composed mostly of individuals who are tax residents in Italy.

In both cases, the presumption is rebuttable : the company can provide evidence to the contrary by demonstrating the actual location of its management and operations abroad. This evidence must be solid and documented: physical headquarters with offices and staff, board meetings held abroad with minutes, contracts signed in the country of incorporation, an active local bank account, and locally maintained accounting records.

Tax evasion and illegal tax evasion

The distinction between the two forms is legally relevant because it affects the applicable sanctions and the criminal relevance:

Tax evasion. This occurs when the foreign company is incorporated with the sole purpose of avoiding Italian taxation, with no economic reason other than the tax advantage. The foreign headquarters is a pure fiction: no offices, no employees, no real activity in the country of incorporation. This is the most serious form: it constitutes a direct violation of tax law and may constitute the crime of false declaration (Article 4, Legislative Decree 74/2000) or, in the most serious cases, fraudulent declaration (Article 3).

Illegal (or tax-evasive) foreign investment. This occurs when the foreign company has a certain real structure but was established or used primarily to obtain an undue tax advantage through a scheme lacking adequate "economic substance." In this case, the rules on abuse of rights apply (Article 10-bis, Law 212/2000, Taxpayer Statute): the tax advantage is disavowed, the taxes are recovered, but the criminal penalty does not apply . The Court of Cassation has clarified (ruling no. 405/2015) that "illegal" foreign investment is punishable only in the presence of "purely artificial" structures lacking any economic justification other than tax savings.

Penalties for foreign investiture: administrative and criminal

Case Law: What the Court of Cassation Says About Foreign Investiture

The Court of Cassation has produced a broad and coherent body of case law on foreign investment. The established principles are:

Substance over form. A company's tax residence is determined by looking at where decisions are actually made, not where its registered office is located (Cass. No. 2869/2013, No. 7080/2014). If strategic decisions are made in Italy, even informally, via email, telephone, or videoconference by individuals resident in Italy, the company is considered Italian.

Nominee directors and nominees. The appointment of a foreign director (nominee director) does not protect against foreign investiture if the decisions are actually made by the Italian shareholder or beneficiary. The Revenue Agency considers "effective management," not the formal position (Cass. No. 2869/2013; Turin Technical Commission, No. 706/2021).

Purely artificial structures. In the EU, reclassification of tax residence is permitted only in the presence of "purely artificial" structures with no economic justification other than the tax advantage. If the foreign company has a genuine economic activity in the country of incorporation, it is not considered a "foreign-inhabited" company (Cadbury Schweppes principle, ECJ C-196/04; Cass. No. 33234/2018).

Burden of proof. In the absence of the presumptions of Article 73, paragraph 5-bis, the burden of proving foreign residency falls on the Revenue Agency. If the presumptions apply (Italian control or a board of directors with an Italian majority), the burden is reversed and the company is responsible for proving actual foreign residency (Cass. No. 32082/2019).

Holding company and strategic vs. operational management. The Court of Cassation distinguishes between group strategic management (typical of the parent holding company) and operational management of the individual subsidiary. The fact that an Italian holding company provides strategic direction to a foreign subsidiary does not automatically imply that the subsidiary is registered abroad, provided that the latter has independent management, its own staff, and actual operations in the foreign country (Court of Cassation no. 33235/2021).

How the tax authorities discover foreign investiture

The Revenue Agency and the Guardia di Finanza have increasingly effective tools for identifying foreign-disguised companies:

Automatic Exchange of Information (CRS/FATCA). Banks in over 100 jurisdictions, including Panama, Switzerland, Singapore, Hong Kong, Belize, and the Seychelles, automatically transmit the financial data of account holders linked to individuals residing in Italy. The Italian Revenue Agency cross-references this data with tax returns and the RW Form .

International cooperation. Through double taxation treaties and Tax Information Exchange Agreements (TIEA), the Italian tax authorities can request detailed information from foreign authorities regarding the structure, operations, and bank accounts of companies suspected of having been acquired abroad.

Risk analysis and data mining. The Italian Revenue Agency uses risk scoring algorithms to identify Italian taxpayers associated with foreign companies in low-tax jurisdictions. The data comes from CRS, FATCA, public company registers, UIF (Financial Intelligence Unit) reports, and information acquired during tax audits.

Inspections and access. The Guardia di Finanza may inspect the Italian premises of taxpayers suspected of having been taxed abroad to obtain documentation (emails, correspondence, contracts, board of directors' minutes, accounting documents) demonstrating the connection between the foreign company and Italy.

Structures most exposed to the risk of foreign investiture

US LLC (Delaware, Wyoming, New Mexico, Florida). The single-member LLC is the most widely used, and most contested, vehicle among Italians for e-commerce, SaaS, dropshipping, freelancing, and international consulting. The risk is real when the sole member is tax resident in Italy and manages the LLC from their Italian domicile: they sign contracts, manage the bank account, respond to clients, and make all operational decisions. To operate properly, the owner must have transferred their tax residency abroad, or the LLC must have independent economic substance in the US.

IBCs and offshore companies (Belize, Seychelles, Nevis, Cook Islands). International Business Companies (IBCs) are particularly vulnerable structures: they often have no offices, employees, or operations in the country of incorporation. If the beneficial owner (UBO) is an Italian tax resident and the company operates as a mere "shell" to hold assets or invoice services, foreign investiture is almost certain.

Panamanian SAs and Private Interest Foundations . Panamanian structures are robust when managed by a Panamanian tax resident, with an active local bank account, RUC , and international economic activity not directed at the Italian market. The risk increases if the partner/founder resides in Italy and makes strategic decisions from Italy.

How to avoid foreign investment: the economic substance requirements

Operating with a foreign company in full legitimacy and free from disputes requires simultaneously meeting formal and substantive requirements. Case law and Revenue Agency practice converge on seven fundamental elements:

1. Actual transfer of tax residence. The shareholder or director managing the company must actually transfer their tax residence abroad: AIRE , deregistration from the Italian registry, and transfer of the center of vital interests to the new country. Without this step, any foreign company managed by an Italian resident is at risk.

2. Effective management headquarters abroad. Strategic decisions must be physically made in the country of incorporation: board meetings held on-site, minutes drawn up and retained abroad, contracts signed in the country. Minutes must be dated, signed, and retained for verifiable purposes.

3. Physical and operational presence. A physical office (not a PO Box), coworking space, or operational headquarters in the country of incorporation. If the business requires it, local staff hired under local contracts.

4. Active bank account with regular transactions. A Panamanian or U.S. account with regular commercial transactions is a strong evidence of substance. A dormant account or one with only domestic transactions has no evidentiary value.

5. Accounting and local compliance. Accounting records kept in the country of incorporation, compliance with local reporting requirements (annual returns, filed financial statements, tax returns), active resident agent, and compliance with corporate taxes.

6. Business targeting foreign markets. If customers, suppliers, and revenue are predominantly Italian, the risk of a hidden permanent establishment in Italy is very high. Business must target international markets, not the domestic Italian market.

7. Overall consistency of the structure. The tax authorities evaluate the overall picture: the owner's residence, company headquarters, bank account, customers, contracts, digital infrastructure (server, domain, hosting). Each element must be consistent with the foreign location. An Italian website, on an Italian server, with content aimed at the Italian market, registered to an Italian entity is a strong indication of foreignization.

Foreign investment and CFC regulations: two distinct disciplines

Those who own foreign companies must distinguish between foreign investment and the regulation of controlled foreign companies (Article 167 of the TUIR). These are two autonomous institutions that may overlap but have different prerequisites and consequences:

The reclassification process concerns the tax residency : the foreign company is reclassified as Italian and taxed fully in Italy on all worldwide income.

The CFC rule concerns the transparency taxation of a foreign company's profits held by the controlling Italian shareholder when the company is located in a country with an effective tax rate lower than 50% of the Italian IRES rate (i.e., lower than 12%) and generates primarily passive income (dividends, royalties, interest, capital gains). The CFC rule applies even if the company is not incorporated abroad.

Practical cases of foreign investiture: calculating penalties

To understand the concrete scope of disputes over foreign investiture, we analyze three typical cases that represent the most frequent situations in professional practice.

Case 1, Italian freelancer with Delaware LLC

A digital marketing consultant residing in Milan establishes an LLC in Delaware (a single-member, disregarded entity for U.S. tax purposes) to bill his services to international clients. He does not transfer his tax residency, does not register with AIRE, and continues to live and work from Italy. The LLC has no offices, employees, or real assets in the U.S. Its annual revenue is €150,000, managed entirely from its Milan domicile.

Dispute: The Revenue Agency determines that the LLC has been registered abroad and reclassifies it as an Italian permanent establishment/sole proprietorship. Calculation of the consequences for a single fiscal year: IRPEF on €150,000 (marginal rate 43%) = approximately €54,000 of tax due. Penalty for failure to file a tax return (120% of the minimum) = €64,800. Unpaid INPS contributions to the separate management system = approximately €36,000. Total for one year: approximately €155,000 , more than the entire turnover. With retroactive assessment over five years: over €750,000 .

Case 2, E-commerce Entrepreneur with IBC Seychelles

An Italian entrepreneur living in Rome establishes an IBC in the Seychelles to operate an e-commerce business selling digital products. The IBC has a bank account in Hong Kong, a website on a Dutch server, and invoices European customers. The entrepreneur manages everything from Italy: he responds to customers, manages the website, coordinates suppliers, and makes all operational and strategic decisions. The IBC has no physical presence in the Seychelles. Annual revenue: €400,000, net profit: €250,000.

Dispute: IBC's foreign tax return. The company is reclassified as resident in Italy. IRES on €250,000 = €60,000. IRAP = approximately €9,750. Unpaid VAT on EU B2C sales = variable but significant. Penalty for failure to file IRES declaration (120%) = €72,000. Penalty for failure to file VAT declaration = additional amounts. Total for one year: over €200,000 . Criminal relevance: IRES tax evaded (€60,000) exceeds the €50,000 threshold → false declaration (Article 4, Legislative Decree 74/2000) , imprisonment from 2 to 4 years and 6 months. With a 5-year assessment: risk exceeding €1 million plus criminal proceedings.

Case 3, Family Holding with SA Panama Properly Managed

An Italian family transfers their tax residency to Panama through the bilateral treaty. The head of the family registers with AIRE , obtains the Cédula E, the DGI tax residency certificate , rents an apartment in Panama City, opens a local bank account , and enrolls their children in an international school. The family actually lives in Panama. They establish a Panamanian SA to hold international real estate and financial investments. The SA has an active resident agent, a corporate account in Panama with regular transactions, locally maintained accounting, and documented board meetings in Panama City.

Result: no risk of foreign taxation. The owner is a tax resident in Panama (no longer resident in Italy), the SA has real economic substance in the country of incorporation, and its effective management is in Panama. The Italian Revenue Agency has no basis to challenge the company's residency. Taxation occurs exclusively in Panama according to the territorial principle: 0% on foreign-source income. Investing in the correct structure—residency + company + account + compliance—costs a fraction of what a single year of tax assessment for foreign taxation would cost.

Foreign Investigation and European Union Law

In the European context, the challenge to foreign-incorporated property is limited by the freedom of establishment enshrined in Articles 49 and 54 of the Treaty on the Functioning of the European Union (TFEU). The Court of Justice of the European Union (CJEU) has developed fundamental principles that govern the application of national anti-foreign-incorporated property laws.

The Cadbury Schweppes principle and purely artificial structures

The Cadbury Schweppes ruling (ECJ, C-196/04, 12 September 2006) established that national anti-abuse laws can limit freedom of establishment only when the foreign company constitutes a wholly artificial arrangement devoid of economic reality. If the foreign company carries out a genuine economic activity in the country of establishment, with premises, staff, equipment, and autonomous decisions, the home Member State cannot challenge its existence solely because it was established to benefit from a more favorable tax regime.

This principle has been endorsed by the Italian Supreme Court (ruling no. 33234/2018) and directly impacts the practice of foreign investiture: a foreign company with genuine economic activity cannot be reclassified as Italian, even if the primary reason for its incorporation is tax advantages. Tax motivation alone is not sufficient to establish foreign investiture within the EU; proof of the artificiality of the structure is required.

Freedom of establishment and choice of jurisdiction

The CJEU has reiterated on several occasions (Centros, C-212/97; Inspire Art, C-167/01; VALE Építési, C-378/10) that a European citizen has the right to freely choose in which Member State to incorporate a company, even if the choice is motivated by a more favorable tax or regulatory regime. This right cannot be limited by the country of origin, unless fraud or abuse is proven.

Panamanian companies , US LLCs , or IBCs in Caribbean jurisdictions, the EU's freedom of establishment does not directly apply. However, the principle of "purely artificial construction" is still used by Italian case law as a benchmark. The Court of Cassation has clarified that even for non-EU companies, foreign incorporation requires proof that the foreign headquarters is fictitious and devoid of any real economic function.

The ATAD Directive and the general anti-abuse clause

Directive 2016/1164 (ATAD, Anti-Tax Avoidance Directive) introduced a general anti-abuse clause (Article 6) applicable to all Member States, according to which a non-genuine arrangement or series of arrangements, implemented for the primary purpose of obtaining a tax advantage, is disregarded. An arrangement is considered "non-genuine" to the extent that it is not implemented for valid commercial reasons that reflect economic reality. Italy has implemented this directive by strengthening Article 10-bis of Law 212/2000 (Taxpayer's Statute) on the regulation of abuse of law, which also applies to cases of "abusive" (non-evasive) foreign tax investiture.

Foreign investiture of natural persons

Foreign residency isn't limited to companies: individuals can also be prosecuted for fictitious foreign residency. The phenomenon is growing rapidly, fueled by the rise of digital nomads, remote workers, and entrepreneurs moving abroad while maintaining significant ties to Italy.

Article 2 of the TUIR: tax residency criteria for individuals

Article 2, paragraph 2, of the TUIR , reformed by Legislative Decree 209/2023, establishes that a natural person is considered tax resident in Italy if, for the majority of the tax period (183 days, even non-consecutive, including fractions of a day), even just one of the following alternative criteria applies: registration in the population registry (from 2024 rebuttable presumption), domicile in the territory of the State (place of personal and family relations) or residence in the territory of the State (physical presence).

The reform introduced two fundamental changes: tax domicile no longer coincides with the place of business and interests (Article 43 of the Civil Code) but with the place of personal and family relations , and registration in the registry office has become a rebuttable presumption, rebuttable by proof to the contrary. This means that an Italian registered with AIRE and formally resident abroad can be considered a tax resident in Italy if the family (spouse, children) lives in Italy, if they maintain a primary residence in Italy, or if their personal relations are concentrated in Italy.

The strengthened presumption for countries with privileged tax systems

Article 2, paragraph 2-bis of the TUIR (Consolidated Income Tax Code) provides a strengthened presumption of Italian residency for citizens who deregister from the registry and move to countries with low tax regimes (pursuant to Ministerial Decree of May 4, 1999). In this case, the burden of proof is reversed: it is the taxpayer who must demonstrate the actual transfer, not the Revenue Agency. Proof to the contrary requires robust documentation: a rental or property agreement abroad, utilities in the taxpayer's name, an active bank account, children's school enrollment, employment contract or business activity in the country, local health card, season tickets, and documented daily expenses.

Recent case law on natural persons

CGT Lombardia – Varese, ruling no. 256/2025: An entrepreneur registered with AIRE and formally resident abroad was deemed to be a tax resident in Italy. His wife and children lived in Italy, the family home was in Italy, the Italian bank accounts were active, and decisions regarding the foreign company were made from the Italian domicile. The result: fictitious foreign residence, full taxation in Italy of all worldwide income, and tax recovery of foreign income.

Turin Provincial Tax Commission, ruling no. 706/2021: A sole director and sole shareholder of a foreign company, officially registered with AIRE, was deemed resident in Italy because he operated permanently from Italy. Commercial and non-accounting documentation found at a related Italian company demonstrated his actual presence in the country. Consequence: both the individual and the company were declared foreign.

Supreme Court of Cassation ruling no. 12259/2010 established that assessing tax residency requires a comprehensive examination of all indicators: demonstrating physical presence abroad is not sufficient if the "center of vital interests"—family, real estate, social relationships, or primary economic interests—remains in Italy. AIRE registration is a formal requirement that does not affect the substantive assessment by the Revenue Agency.

These cases confirm a clear principle: for individuals, as well as for companies, the transfer of tax residency must be real, complete, and documentable . Those who move to Panama with their family, actually live in the country, shift the focus of their personal and family relationships outside of Italy, and document each step with objective evidence are in a solid position. Those who register with AIRE but leave their family in Italy, keep their home and active bank accounts, and continue to operate from Italy risk being challenged for fictitious residency, with consequences identical to those of corporate investiture.

The five mistakes that expose you to investigation

1. Open a US LLC or an offshore IBC while remaining resident in Italy , believing that a foreign registered office is sufficient. This isn't the case: the tax authorities look at where decisions are made, not where the company is registered.

2. Appointing a foreign nominee director in the belief that this will shift effective management abroad. The Revenue Agency verifies who actually makes decisions, not who formally signs.

3. Dealing with Italian customers and suppliers through the foreign company , creating a hidden permanent establishment in Italy. If the turnover is predominantly Italian, the company is considered operating in Italy.

4. Register the website and domain name in the name of an Italian entity , with hosting on Italian servers and content in Italian aimed at the domestic market. This is a demonstrable indication of foreign ownership.

5. Do not request a certificate of tax residency in the foreign country and do not document the company's economic substance. Without positive evidence of foreign operations, the Revenue Agency has an easy time contesting the foreign tax return.

Reference legislation and practices

The regulatory framework for foreign investiture is structured on three levels: domestic law, international conventions, and EU law, which interact with each other and must be assessed jointly in each specific case.

Italian domestic law

Article 73, paragraph 3, TUIR (Presidential Decree 917/1986, as amended by Article 2, Legislative Decree 209/2023): tax residency criteria for companies: registered office, place of effective management, ordinary management through the principal branch. Article 73, paragraph 5-bis, TUIR (introduced by Legislative Decree 223/2006): rebuttable presumptions of residency for foreign companies controlled by Italian entities or with a board of directors with an Italian majority. Article 2, paragraph 2, TUIR (reformed by Legislative Decree 209/2023): tax residency criteria for natural persons: registration, domicile, residence. Article 2, paragraph 2-bis, TUIR : strengthened presumption for transfers to countries with privileged tax regimes. Article 167, TUIR : regulation of CFCs (Controlled Foreign Companies). Article 162, TUIR : definition of permanent establishment. Article 10-bis, Law 212/2000 (Taxpayer Statute): rules governing abuse of rights. Article 4, Legislative Decree 74/2000 : false declaration, criminal liability for evaded taxes exceeding €50,000. Article 3, Legislative Decree 74/2000 : fraudulent declaration through other means.

Revenue Agency Practices

Circular 20/E of November 4, 2024: operational clarifications on the new tax residency criteria introduced by Legislative Decree 209/2023, with definitions of "place of effective management" and "ordinary management in the principal place," practical examples on counting 183 days, and information on fractions of a day. Circular 34/E of 2009: interpretation of corporate residency criteria and indicators of foreign tax residency. Circular 6/E of 2016: clarifications on CFC regulations and their relationship with foreign tax residency.

Relevant case law

Cass. No. 2869/2013: substance prevails over form in determining the place of effective management. Cass. No. 7080/2014: the formal registered office is irrelevant when management is in Italy. Cass. No. 33234/2018: implementation of the Cadbury Schweppes principle, need for "pure artifice" to challenge freedom of establishment. Cass. No. 33235/2021: distinction between strategic management of the group and operational management of the foreign subsidiary. Cass. No. 32082/2019: burden of proof in the absence and presence of presumptions pursuant to art. 73, paragraph 5-bis. CTP Turin No. 706/2021: foreignization of a company with a sole director registered with AIRE but operating from Italy. CGT Lombardia – Varese No. 256/2025: Fictitious residence abroad of a natural person with family in Italy.

European Union Law and International Conventions

Articles 49 and 54 TFEU: freedom of establishment. Directive 2016/1164/EU (ATAD): general anti-abuse clause and harmonized CFC rules. ECJ C-196/04 (Cadbury Schweppes): anti-abuse rules can limit freedom of establishment only in the case of "purely artificial arrangements." ECJ C-212/97 (Centros): right to incorporate a company in the Member State with the most favorable regime. ECJ C-167/01 (Inspire Art): confirmation of the right to choose jurisdiction, including for tax reasons. OECD Model: Art. 4, definition of tax residence and tie-breaker rules for residence conflicts; Art. 5, permanent establishment. The bilateral double taxation treaties signed by Italy (over 90) apply these criteria to specific cases.

Compliant offshore structuring: specialized consultancy

Studio Panama Italia assists Italian entrepreneurs and investors in structuring foreign companies in compliance with Italian and international regulations. From incorporation to economic substance management, from CFC compliance to transferring tax residency to Panama, each structure is designed to withstand an audit. We have been operating from Panama City since 2010, license no. 14465.

✉️ Write to us on WhatsAppFrequently asked questions about foreign investiture

What is foreign investiture in simple terms?

Foreign tax investiture occurs when a company is registered abroad but managed from Italy. The Italian tax authorities consider it an Italian company disguised as a foreign one and tax it on all worldwide income, applying penalties ranging from 120% to 240% of the evaded tax.

Is it illegal to open a company abroad?

No. Establishing and managing a foreign company is perfectly legal. Foreign taxation only occurs when the company is used as a front to evade Italian taxation, with no economic substance in the country of incorporation and effective management from Italy.

If I move my tax residency to Panama, is my US LLC at risk?

No, provided the transfer is effective and documented. If the partner/director is a Panamanian tax resident (AIRE registration, DGI certificate, and actual residence in the country), the US LLC is managed by a non-Italian resident and the risk of foreign ownership of the company in Italy is eliminated. CFC compliance and applicable US regulations must still be verified.

Does a nominee director protect against foreign investiture?

No. Appointing a nominee isn't sufficient if the decisions are actually made by the Italian partner. The Revenue Agency and the Supreme Court of Cassation look at the substance, who actually makes the decisions, not the formal role. A nominee without real decision-making power is evidence of foreign ownership, not protection.

What are the penalties for foreign investment?

Administrative penalties: IRES (24%) and IRAP (3.9%) on all worldwide income, plus a penalty ranging from 120% to 240% of the evaded taxes. Criminal penalties: If the evaded tax exceeds €50,000 per year, the offense of false tax filing is considered (Article 4, Legislative Decree 74/2000, imprisonment from 2 to 4 years and 6 months). For higher amounts with false invoices: fraudulent tax filing (Article 3), imprisonment from 4 to 8 years.

How to demonstrate the economic substance of a foreign company?

Through: a physical office in the country of incorporation, an active bank account with regular business transactions, minutes of board meetings drafted and signed locally, contracts signed in the country, local personnel (if applicable), up-to-date local accounting and compliance, and a tax residency certificate issued by the foreign country's authority. All of these elements must be consistent and verifiable.

What is the difference between foreign investment and CFC legislation?

The "foreign investment" rule concerns the company's tax residency: the foreign company is reclassified as Italian and taxed fully in Italy. The CFC rule (Article 167 of the Consolidated Income Tax Code) concerns the transparency taxation of profits for the Italian shareholder when the company is located in a low-tax country and generates passive income. These two autonomous rules can coexist.

Is Panama a country at risk of foreign investiture?

No, if the structure is properly set up. Panama has been on the OECD White List since 2023, which reduces the level of scrutiny. A Panamanian company managed by a tax resident in Panama, with an active bank account, office, and real business, is not at risk. The risk exists if the owner resides in Italy and manages the company from Italian territory.

Learn how to obtain Panamanian residency in 6 steps , register with AIRE , obtain a tax residency certificate , open a company in Panama , and open an offshore account in Panama asset protection structures and private interest foundations , consult the dedicated guides.