AIRE Registration for Italians Abroad — Complete Guide 2026

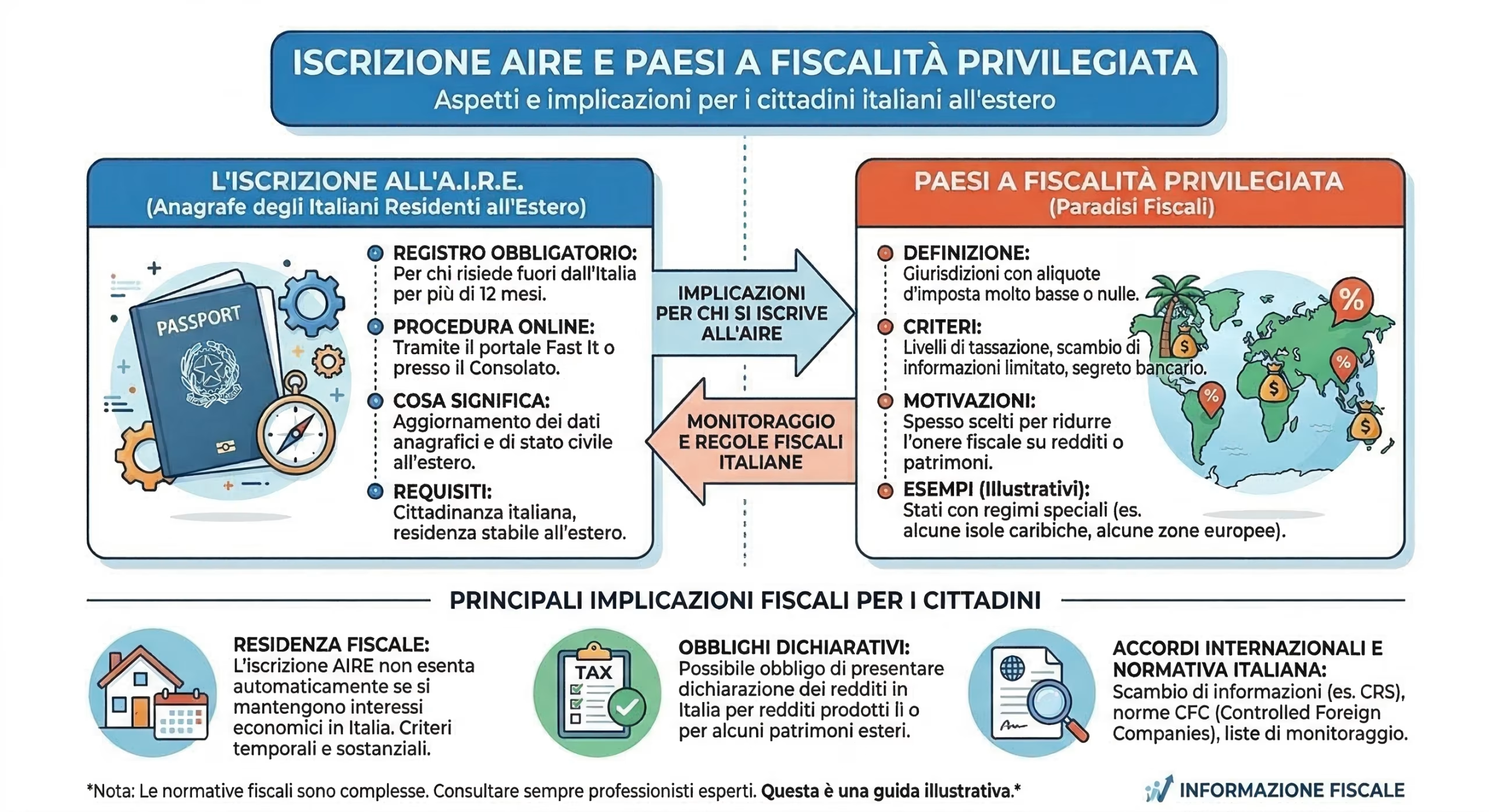

Registration with AIRE (Registry of Italians Resident Abroad) is the first formality every Italian citizen must complete when transferring their residence abroad. It is not a secondary bureaucratic formality: AIRE registration is the legal prerequisite for removal from the registry of the Italian municipality of origin, for the cessation of Italian tax residency, and for access to all civil and consular rights abroad. Without AIRE, for Italian tax purposes, you are still resident in Italy—with the obligation to declare and tax worldwide income at the standard IRPEF rates, which in 2026 reach 43% for income exceeding €50,000, plus additional regional and municipal taxes.

This guide—updated to Law No. 11 of January 19, 2026 —explains in detail what AIRE is, who is required to register, how to register (online and at the Consulate), the tax consequences of registration and non-registration, the rulings of the Court of Cassation, and how AIRE registration fits into the process of moving to Panama and other countries with territorial taxation.

Key points

- What is AIRE: Registry of Italians Residing Abroad, established by Law 470/1988, a mandatory register for those residing outside Italy for more than 12 months

- Registration requirement: within 90 days of moving residence abroad (Article 6, Law 470/1988)

- How to register: Fast It portal of the Ministry of Foreign Affairs (SPID, CIE) or directly at the competent Consulate

- Cost: Free — no cost for AIRE registration

- Penalties for failure to register: from €200 to €1,000 for each year of failure (Law 213/2023, effective from 2024)

- New for 2026: Law 11/2026 (effective from 19 February 2026) introduces new provisions on registration methods, CIE abroad and excluded categories

- Tax effect: necessary (but not sufficient) condition for the cessation of Italian tax residency - the Court of Cassation evaluates the center of vital interests

- For those moving to Panama: AIRE registration + DGI certificate complete the fiscal transfer to 0% territorial taxation.

What is AIRE and why does it exist?

AIRE was established by Law No. 470 of October 27, 1988 , and its implementing regulation (Presidential Decree No. 323 of September 6, 1989). It is a registry managed by Italian municipalities that collects the data of Italian citizens permanently residing abroad for a period of more than 12 months. AIRE is centrally coordinated by the Ministry of the Interior and, since 2022, has been merged into the ANPR (National Registry of the Resident Population), the single national database managed by the Ministry of the Interior that unifies AIRE and APR (Registry of the Resident Population). The registry is updated through reports from Italian consulates around the world.

AIRE registration has effects on three distinct levels: registry (cancellation from the municipality's resident population register), tax (termination of the presumption of Italian tax residency), and civil (exercise of the right to vote abroad, access to consular services, and renewal of documents). For those moving to Panama through the bilateral treaty , AIRE registration transforms migratory residency into an effective fiscal transfer, paving the way for Panamanian territorial taxation with a 0% rate on foreign-source income.

Who is required to register with AIRE?

The registration requirement applies to all Italian citizens who transfer their residence abroad for a period exceeding 12 months, or who already reside permanently abroad. Specifically, the following are required: employees transferred abroad by their employer or by personal choice, entrepreneurs who move their primary focus outside of Italy, self-employed professionals and freelancers who operate permanently from abroad, retirees who are relocating permanently, digital nomads who elect domicile in another country, spouses and minor children accompanying the transferee, Italian citizens born abroad who have never been registered in an Italian municipality, and citizens who acquired Italian citizenship by jus sanguinis but reside permanently outside of Italy.

Subjects exempt from registration

The following individuals are not required to register with AIRE: permanent state employees serving abroad pursuant to the Vienna Conventions on Diplomatic Relations (1961) and Consular Relations (1963), Italian military personnel serving at NATO offices and facilities abroad, and officials of international organizations enjoying diplomatic immunities. Those traveling abroad for temporary stays of less than 12 months (study, seasonal work, tourism, internships) are not subject to the requirement. Law 11/2026 further clarified the excluded categories, introducing the possibility of optional AIRE registration for citizens with tax domicile in Italy who work abroad at European Union facilities or other international organizations.

How to register with AIRE: 2026 procedure

Registration can be done through two channels. In both cases, it is essential to submit the application within 90 days of transferring residence abroad, as required by Article 6 of Law 470/1988.

Fast It Portal of the Ministry of Foreign Affairs (online)

The main channel is the Fast It (Farnesina Telematic Services for Italians Abroad) online portal, accessible at serviziconsolarionline.esteri.it with SPID, CIE, or CNS. The procedure requires completing the digital form with complete personal details and foreign address of residence, uploading a valid identity document (passport or CIE), documentation proving residence abroad (rental contract, utility bills, local residence certificate), and indicating the competent Consulate for the area. Once the application is submitted, the competent Consulate carries out the verification—which can take from a few weeks to several months depending on the Consulate—and forwards the notification to the Italian municipality of last residence for cancellation from the APR.

Direct presentation to the Consulate

Alternatively, you can apply in person to the Italian Consulate responsible for your country of residence with a valid passport or Italian identity card, tax code, and proof of residence in the foreign country (rental agreement, utilities, or local residence certificate). If you do not have Italian documents, a foreign identity document with all necessary personal information will be accepted. The Consulate will register the applicant in the consular register and notify the Italian municipality for deregistration from the APR. AIRE registration can also be completed automatically, once the Consulate becomes aware of the citizen's move.

For those moving to Panama, the competent consulate is the Consulate General of Italy in Panama City . Our legal assistance includes support for AIRE registration as part of the complete Panama residency package .

New for 2026: Law 11/2026

Law no. 11 of 19 January 2026 , which came into force on 19 February 2026 , introduced important changes for Italians residing abroad:

New AIRE registration procedures. The law updates the registration and data reporting procedures, aligning them with the ANPR system and providing for integration with public administration digital services.

Electronic Identity Card (CIE) abroad. Starting June 1, 2026, all Italian citizens registered with AIRE will be able to apply for the new CIE not only at their local consulate, but also at any Italian municipality during temporary stays in Italy. The CIE contains the tax code and fingerprints and can be used to access online public administration services (the alternative SPID) and for digital signatures.

Passports. Passports can no longer be "renewed": upon expiration, they must be requested as new documents at the Consular Offices.

Categories Excluded from Registration. The law specifies the categories exempt from the requirement, reaffirming the concept of a connection to Italy for temporary activities, and introduces optional registration for employees of EU institutions and international organizations with tax domicile in Italy.

Registration terms and penalties

Article 6 of Law 470/1988 requires registration within 90 days of transferring residence abroad. From 2024, with the entry into force of Law No. 213 of December 30, 2023 (2024 Budget Law, Article 1, paragraph 242), failure to register with AIRE will result in an administrative fine ranging from €200 to €1,000 for each year of omission , up to a maximum of €5,000 overall . Fines are imposed by the Municipality of the person's last residence in Italy.

This is a significant change: until 2023, there was no specific penalty for failure to register, which had led to a widespread phenomenon of Italians residing abroad but never being removed from the municipal registry. The penalty, introduced in 2024, aims to align the registry with the actual situation and prevent the phenomenon of "fictitious residence" in Italy.

Tax consequences of AIRE registration

AIRE registration is a necessary but not sufficient for ceasing Italian tax residency. This is the cornerstone of the matter, reaffirmed by the Court of Cassation through decades of consistent case law. Article 2, paragraph 2, of the TUIR (Presidential Decree 917/1986) establishes that an individual is considered tax resident in Italy if, for the majority of the tax period (183 days, even non-consecutive, considering fractions of days), even just one of the following alternative criteria is met:

1. Registration in the Resident Population Registry. Since 2024, following the amendments introduced by Legislative Decree 209/2023, registration in the Registry has become a rebuttable , rebuttable by proof to the contrary. Before 2024, it was an absolute presumption: registration in the Registry alone automatically established Italian tax residency. Today, AIRE registration still carries significant weight, but is not in itself decisive if rebutted by substantial evidence.

2. Domicile within the territory of the State. For the purposes of the TUIR (Income Tax Code) as amended by Legislative Decree 209/2023, domicile coincides with the place where personal and family relationships . This definition replaced the previous reference in the Civil Code (Article 43 of the Civil Code) and shifts the focus from the place of business and interests to personal relationships: family, children, social ties, and daily life.

3. Residence in the Italian territory. Residence is defined as physical presence in Italy for the majority of the tax period. The calculation includes fractions of a day: even a single hour spent in Italy on a given day is counted.

The jurisprudence of the Supreme Court: what really matters

The Court of Cassation has developed a consolidated approach regarding AIRE and tax residency. The most relevant rulings are:

Cass. No. 13803/2001: established that tax domicile is independent of physical presence and coincides with the place where an individual intends to establish and maintain the center of their economic, social, and family interests. AIRE registration is a formal requirement that does not affect the substantive assessment.

Cass. No. 10179/2003: confirmed that cancellation from the Italian registry and AIRE registration are not sufficient to exclude tax residency if the taxpayer maintains his or her center of vital interests in Italy.

Cass. Nos. 14436/2010 and 12259/2010 reiterated that the tax authorities evaluate the taxpayer's "complex interests"—economic, patrimonial, family, and social—rather than the individual formal element. The presence of family, real estate, active bank accounts, and corporate positions in Italy are indicators that the Revenue Agency uses to challenge the transfer.

CGT Lombardia – Varese, ruling no. 256/2025: A recent ruling reaffirmed the principle: a taxpayer registered with AIRE and formally resident abroad was considered tax resident in Italy because his wife and children lived in Italy, the family home was in Italy, and decisions regarding the foreign company were made in Italy. The result: fictitious foreign residency, full taxation in Italy, and tax recovery of foreign income.

What's changing from 2024: Legislative Decree 209/2023

Legislative Decree 209/2023 (international tax reform) has profoundly changed the criteria for determining the tax residency of individuals, effective from the 2024 tax period:

Rebuttable presumption. Registration in the Italian population registry is now a rebuttable presumption, no longer an absolute one. This means that a taxpayer registered in the Italian registry can demonstrate that they are tax resident abroad (and vice versa: an AIRE member can be considered resident in Italy if the substantive requirements are met).

Redefined domicile. Tax domicile is no longer identified with the principal place of business and interests (art. 43 of the Civil Code) but with the place of personal and family relations . This shift makes it more difficult for those with family in Italy to maintain foreign tax residency.

Counting days. Fractions of days are also counted. An airport transit lasting a few hours in Italy is counted. Circular 20/E of the Revenue Agency (November 4, 2024) provided practical examples of the calculation.

For Italian citizens transferring their tax residency to Panama, these changes reinforce the need for an effective and complete : simply registering with AIRE and obtaining the Cédula E is not enough. Life must actually take place in Panama—address, utilities, bank account, family relationships, economic activity—and ties with Italy must be kept to a minimum.

AIRE and countries with privileged tax systems: the strengthened presumption

Article 2, paragraph 2-bis of the TUIR (Consolidated Income Tax Code) provides a strengthened presumption of Italian tax residency for Italian citizens who deregister from the Italian registry and move to countries with privileged tax regimes (pursuant to Ministerial Decree of May 4, 1999, and subsequent amendments). For these taxpayers, the burden of proof is reversed: it is the taxpayer—not the Revenue Agency—who must demonstrate that the transfer is genuine and not fictitious. Proof to the contrary can be provided through: employment contracts abroad, availability of a stable residence, registration with local registry offices, and documentation relating to utilities, financial status, and personal relationships in the destination country.

AIRE registration for those moving to Panama

For Italian citizens who obtain residency in Panama through the Italy-Panama Treaty of Friendship, Commerce, and Navigation (Law 15 of February 1, 1966) , the AIRE registration process follows a specific path. Once the migration procedure has been completed at the National Migration Service and the migration carnet (and subsequently the Cédula E issued by the Electoral Tribunal) has been obtained, the Italian citizen can register with AIRE at the Italian Consulate General in Panama City by presenting the Panamanian residency documentation: passport, Cédula E, rental agreement, and utilities in their name.

AIRE registration at the Panamanian Consulate entails deletion from the registry of the Italian municipality and, combined with the tax residency certificate issued by the Panamanian Directorate General of Income (DGI), completes the tax transfer from Italy to Panama. From that moment, the taxpayer is subject exclusively to Panamanian territorial taxation : zero taxes on foreign-source income, including remote work, private pensions, international dividends, capital gains, royalties, and cryptocurrencies.

The complete supporting documentation for a move to Panama includes: a definitive migration carnet, Cédula E, AIRE registration, DGI tax residency certificate, rental agreement or property title, an active bank account in Panama with regular transactions, utilities in your name (electricity, internet, water), and—if applicable— Panamanian company with RUC .

After AIRE registration: what happens in Italy?

Loss of Italian healthcare

AIRE registration entails the loss of the right to healthcare through the Italian National Health Service (SSN). The health card is deactivated, and the citizen can no longer access free medical services in Italy, except for urgent services during temporary stays. Starting in 2026, the Budget Law confirmed the possibility for AIRE members residing in non-EU countries to request a health card for temporary stays in Italy, upon payment of an annual flat fee.

Panama's private healthcare system is excellent: Punta Pacífica Hospital (a Johns Hopkins Aetna affiliate), the National Hospital, and the Paitilla Medical Center offer international standards. The cost of comprehensive private health insurance in Panama ranges from $150 to $400 per month, depending on age and coverage. The Pensionado also offers significant discounts (15-25%) on medical services, medications, and specialist consultations.

Residual taxes in Italy for non-residents

Once the transfer of tax residence has been completed (AIRE registration + actual transfer of the center of vital interests), the taxpayer is no longer required to declare worldwide income in Italy. However, some Italian tax obligations remain for those who maintain assets in Italy:

Real estate in Italy: IMU remains due on properties owned in Italy (with the benefits available to AIRE members: exemption for unrented properties not loaned for use, if provided by the municipality). TARI is due if the property has active utilities.

Income from Italian sources: Real estate rentals in Italy, fees for activities carried out in Italy, and income from investments in Italian companies remain taxable in Italy, even for non-residents. The Italy-Panama Double Taxation Convention applies to avoid double taxation.

RW Form and IVAFE/IVIE : The obligation to monitor foreign assets (accounts, companies, real estate outside Italy) ceases completely upon transferring tax residency abroad. Those registered with AIRE and tax resident in Panama are not required to complete the RW Form or pay IVAFE or IVIE.

Rights and services for AIRE members

AIRE registration guarantees access to essential services: exercising the right to vote by mail in parliamentary, European, and referendum elections (Law 459/2001); passport and identity card renewal at the competent Consulate; issuance of registry and civil status certificates; the option of having notarial deeds executed through the Consulate; and access to a health card for temporary stays in Italy (from 2026, subject to a flat-rate fee for AIRE members in non-EU countries). Starting June 1, 2026, thanks to Law 11/2026, the CIE can also be requested in any Italian municipality during temporary stays, not just at the Consulate.

Cancellation from AIRE and repatriation

AIRE registration is cancelled in the following cases: registration in the Resident Population Registry (APR) of an Italian municipality following repatriation, death (including judicially declared presumed death), presumed untraceability (after 100 years have passed since birth or after two subsequent unsuccessful checks, or when the foreign address is no longer valid and it is not possible to acquire a new one). Anyone returning to Italy must go directly to the municipality of destination to declare their new address—the Consulate is not responsible for repatriation procedures.

Common mistakes to avoid

The five most common mistakes we encounter in our legal practice are: 1. Delaying AIRE registration beyond 90 days, exposing oneself to penalties and tax disputes. 2. Maintaining Italian residency "as a precaution" or to retain a primary care physician—which nullifies the tax transfer and leaves the taxpayer subject to worldwide income tax (IRPEF). 3. Failing to collect documentary evidence of actual residence abroad: rental agreement, utilities in one's name, bank transactions, local invoices, airline tickets. 4. Maintaining family in Italy (spouse, children) while registered with AIRE—this is the strongest indication of fictitious residency according to case law. 5. Failing to apply for a tax residency certificate in the new country (the DGI certificate in Panama)—without this document, the tax transfer is weak and open to challenge.

Assistance with moving to Panama and AIRE registration

Studio Panama Italia assists Italian citizens through every stage of their relocation: from the residency process under the Italy-Panama Treaty, to opening a bank account, to registering with the Italian Registry of Italian Territories (AIRE) and obtaining the DGI tax residency certificate. We have been operating from Panama City since 2010 with license no. 14465.

✉️ Write to us on WhatsAppFrequently asked questions about AIRE registration

Is AIRE registration mandatory for those moving to Panama?

Yes. Registration is required by law (Law 470/1988) within 90 days of moving for any Italian citizen residing abroad for more than 12 months. For those moving to Panama, AIRE registration at the Consulate in Panama City is also a prerequisite for Italy to recognize Panamanian tax residency.

Can I register with AIRE online?

Yes, through the Ministry of Foreign Affairs' Fast It portal, accessible with SPID, CIE, or CNS. Submitting the application does not automatically mean acceptance: the application is verified by the relevant Consulate, which may require additional documentation. Processing times vary from a few weeks to several months.

What happens if I don't register with AIRE?

Starting in 2024, penalties ranging from €200 to €1,000 will apply for each year of failure to register, up to a maximum of €5,000. For tax purposes, failure to register implies continued Italian tax residency, requiring all worldwide income to be declared and taxed in Italy at IRPEF rates (up to 43%).

Is AIRE registration sufficient to avoid paying taxes in Italy?

No. AIRE registration is a necessary but not sufficient condition. The Court of Cassation (rulings no. 13803/2001, 10179/2003, 14436/2010, 12259/2010) has established that the tax authorities evaluate the taxpayer's center of vital interests: family, economic relationships, real estate, bank accounts. The transfer must be substantial and documentable, not merely formal. Since 2024, Legislative Decree 209/2023 has made registration a rebuttable presumption, rebuttable by proof to the contrary.

How much does AIRE registration cost?

AIRE registration is completely free. There are no fees charged by the Consulate or Municipality. Any associated costs include translation and apostille of foreign documents, if required by the relevant Consulate.

Can Italy still tax me after I move to Panama?

Yes, if the transfer is not effective and documentable. Article 2, paragraph 2-bis of the TUIR (Consolidated Income Tax Code) provides for enhanced controls for transfers to low-tax countries. Panama left the Black List in 2023 (OECD White List), which means the burden of proof falls on the Revenue Agency, not the taxpayer. However, in the first few years after the transfer, it is essential to retain all supporting documentation.

What happens to Italian health insurance with AIRE registration?

Access to the Italian National Health Service (NHS) is lost, except for urgent medical services during temporary stays. Starting in 2026, AIRE members in non-EU countries can apply for a health card for stays in Italy, subject to an annual flat fee. Panama has an excellent private healthcare system: Punta Pacífica Hospital (a Johns Hopkins affiliate), National Hospital, and Paitilla Medical Center.

If I keep a house in Italy, am I at risk of tax disputes?

Yes. A property owned in Italy, especially if it's a primary residence, can be interpreted by the Revenue Agency as evidence of the center of vital interests. It's advisable to sell or rent the property before transferring, or to provide clear documentation that the primary residence is in Panama and that the Italian property is held exclusively as an investment.

Does AIRE registration have retroactive effect?

No. AIRE registration takes effect from the date of the request (Article 7, Presidential Decree 323/1989), not from the date of actual transfer. For this reason, it is essential to submit the application within the 90 days required by law: a delay in registration may leave the interim period uncovered, during which the taxpayer is still considered a full resident in Italy.

I work remotely for a foreign company while living in Panama: where do I pay taxes?

If your tax residence is in Panama (AIRE registration + DGI certificate), income from remote work for a foreign company is not taxable in Panama because the income is not Panamanian-sourced (territorial taxation). It is also not taxable in Italy because you are a non-resident. It is necessary to check the regulations of the country where the company is based to rule out residual tax obligations and permanent establishment arrangements.

Also learn how to obtain Panamanian residency in 6 steps , obtain a tax residency certificate , open a company in Panama , open an offshore bank account in Panama , or obtain Panamanian citizenship and a passport . For asset protection and Private Interest Foundations , consult the dedicated guides.